Don't ask the group chat for permission

Consensus and price, NYRF #2, Delve, Security

I had a conversation with an investor managing a large institution and many billions of dollars this week. This guy is, by any measure, orders of magnitude more successful than I am and pushed hard/called bullshit on some of my usual talking points.

He’s not gonna read this but I’d still like to state my case a little more eloquently than I did IRL, especially in light of “the group chat” essay which is cynical, distasteful, and completely true.

Cheap like expensive is neither inherently good nor bad. A business is just a business, and price at seed is mostly a reflection of the market, not inherent worth. Remember, any reasonable DCF/the true FMV of every early-stage investment is approximately zero.

Believing that something being out of favor makes it good is just as specious and lazy as the opposite belief: that something being expensive makes it good. In either case, you’re outsourcing judgment to others.

Is there any objective measure of (non-) consenus? Obviously yes but also no, not really.

“Non consensus” can either be an input (price) or process (judgement).

In the former, you’re agknowledging/claiming that only way for something to be non-consensus is for it to be cheap. The idea of being a “contrarian” while paying top quartile prices is obviously insane nonsense.

Conversely/in the latter, you’re focused deriving a judgement/value of a business irrespective of what others think (how hot-or-not it is). That will sometimes mean paying up!

It’s easy to hate paying high prices but do you have the courage to hate paying low prices?

With enough companies/a big enough sample, the two ideas should converge at the median and diverge at the average (you might independently conclude Anthropic really is that good and be right!).

In an industry/asset class with power law outcomes, it’s totally reasonable to pay multiples more for the 99th percentile than the 90th percentile of quality opportunities, but caveat emptor. Distinguishing between those without real meaningful data beyond what others think is basically impossible or, at the very least, approximates to a random walk.

If I have one core insight and belief at seed/pre-seed, it’s this: there’s a huge amount of false precision and unreasonable confidence in assessing the best, the worst, and the median opportunities.

What “everybody knows,” what “the group chat decides,” and what’s actually true are not a perfect circle even if it feels really good to believe that they are.

From Kingmaking and the limits of external conviction:

King making is permission-based; it only works on the basis of elite buy-in/consensus […]

At Slow, we believe deeply in founder-led/internal paths to conviction. Whether that happens heads-down in a notebook (calling your shot) or heads-up in the market (calling your customer) doesn’t matter. We can fund you to conviction/insight or meet you once you have it. But it has to come from you, not us.

“The group chat” is externally derived conviction and is highly permissioned and better suited to those who need permission to build and buy.

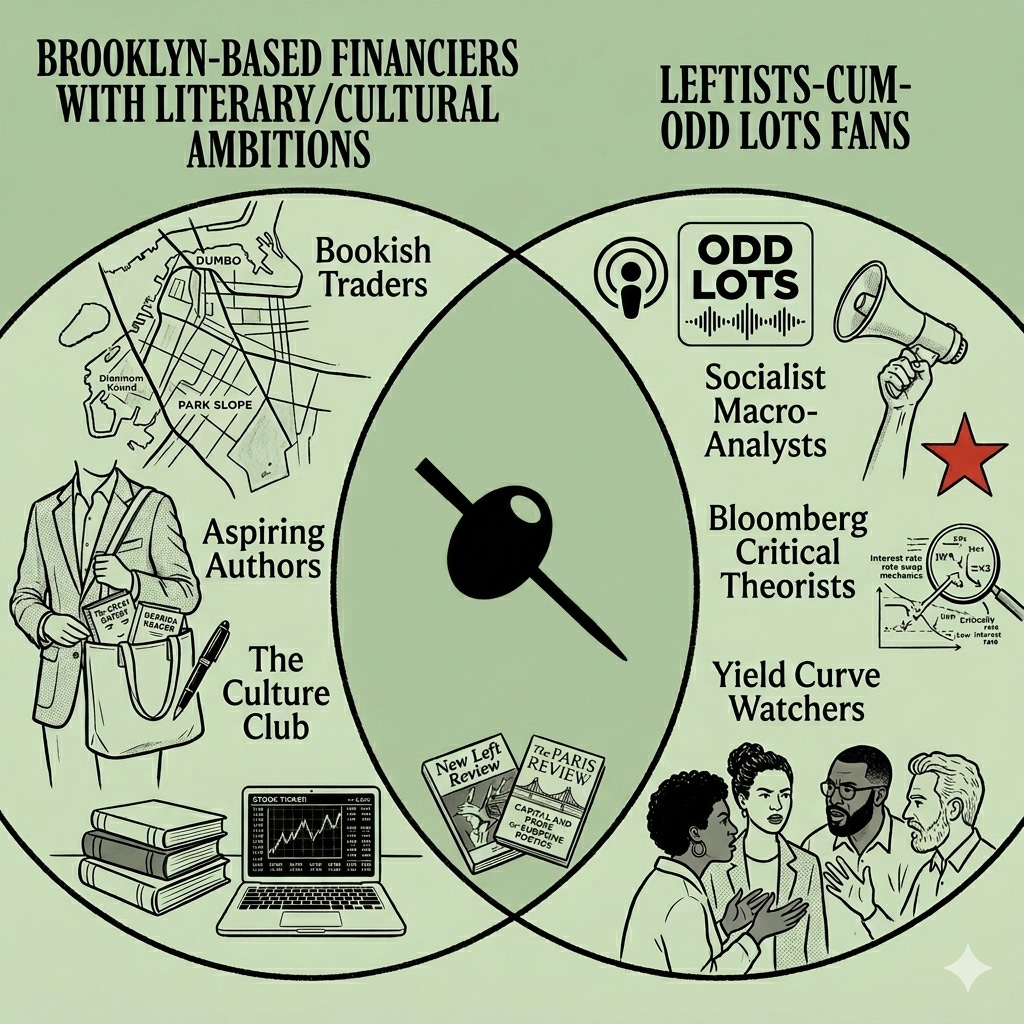

A New York financier reviews New York Review of Finance

This morning I got the second edition of NYRF delivered in print to my door. It’s great and I like the un-accredited writing in the style of The Economist. It creates the impression that you’re peaking behind the curtain of what folks are ~~really~~ saying but can’t say...

A lot of reads a bit too skeptical and incurious about tech (a preemptive elegy for AI is a bit on the nose) but that is probably the perfect center of the venn diagram between NY financiers living in Brooklyn and harboring literary/cultural ambitions and leftists-cum-Odd-Lots-fans who are reading and writing this (guilty as charged). Excited to see the next quarterly edition.

The art direction is great down to the partners they’ve chosen to work with as advertisers.

Notes

This is a really fantastic slide from Redpoint’s market update deck/post.

YC quietly removed delve from its directory without issuing a public statement. I really don’t get who that’s for/that seems like the most mealy-mouthed, worst version of a comms strategy. Stand by your guy or don’t, especially if you want to be the self-proclaimed moral voice of tech, as Garry does. ICYMI Delve did a big fraud on a bunch of other startups (allegedly) and might be at least partially responsible for the Mercor hack... bad!

GLP-1s are a bigger business than AI. Continue to watch this space. Were it not for AI, they would be widely viewed as the most important thing in the world right now.

One of my favorite posters posits that maybe only 3 jobs: innovators, marketers, and context carriers. Personally I prefer my four jobs but he makes good points 😉

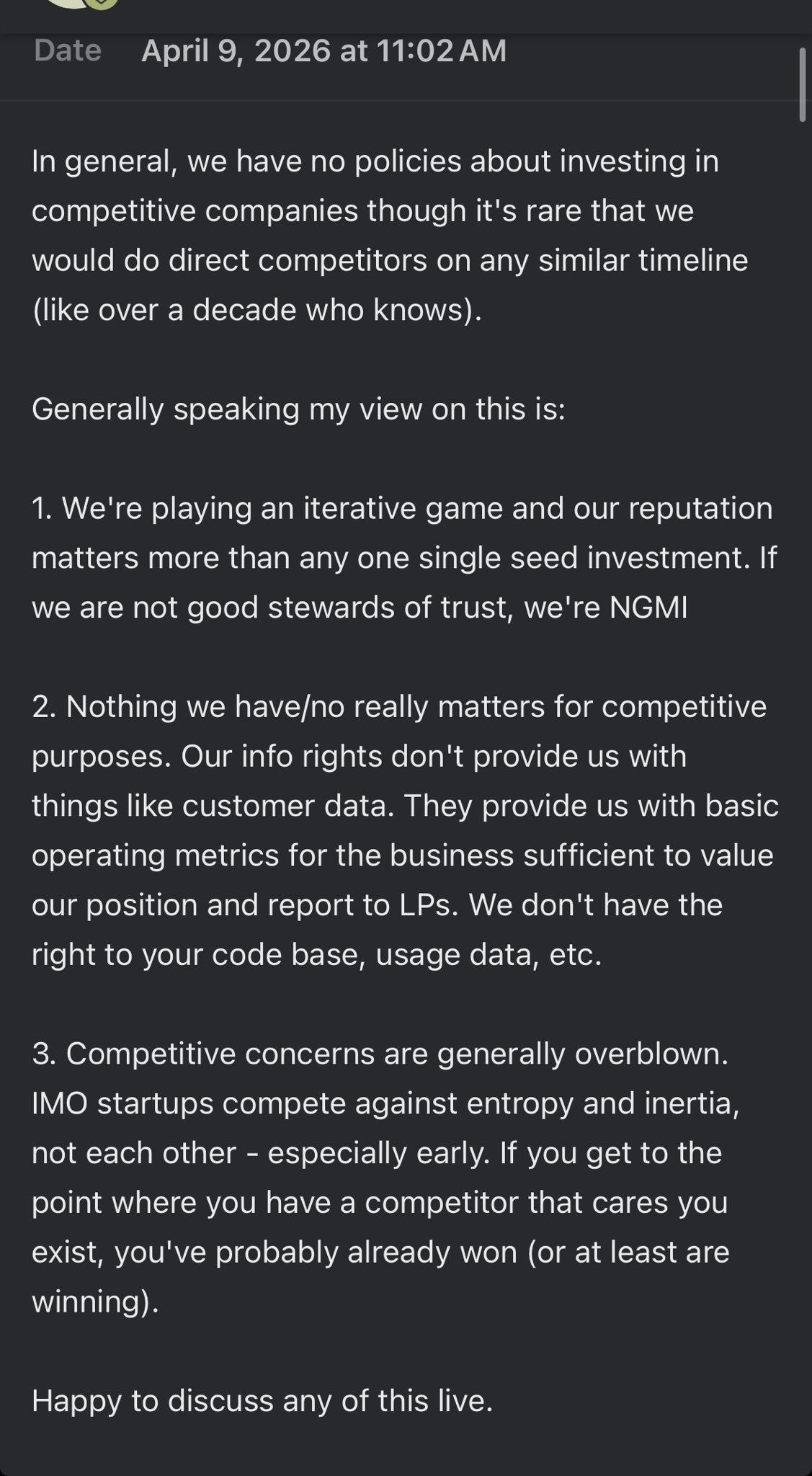

A note on competition/conflicts:

Here’s an email I wrote to a founder on how we think about investing in competitive companies (which, in fairness, we basically never do). Some people got Big Mad at me online which felt fairly performative - just another salvo in the fight to prove (to whom idk) that you’re The Most Founder Friendly...

To me the takeaway is actually fairly positive sum: companies don’t really succeed and fail on the basis of some competitor, at least not until they’re much further along. We don’t need to kill the other crabs to escape from the bucket.

Slow Security

Super stoked for this: we’re hosting founders, operators, security leaders for a ≈100 person cyber security mini conference in NY next month.

We’ll have Anthropic’s head cyber and NatSec policy for a fireside chat and panels with some excellent security operators and investors.

Sign up to join us. Space is limited and we want to prioritize builders and buyers.