Role Modeling

Beware, what follows is a post on startup financial modeling/ analysis. Bear in mind, I have no formal finance education. Proceed at your own risk. You asked for this.

When a startup gives you numbers, how do you assess what’s real, what’s good, what’s bad, and what’s possible? How should you think about not just how the business looks like today, but what could it look like in the future? It takes critical thinking, good judgement, and some pattern matching/experience. But to put that thinking to work, you have to first be able to structure your thoughts and see the picture clearly.

There’s tremendous value in model making as an analytical rather than predictive tool.

When I’m modeling, my goal is usually not to determine what will happen, but rather to understand what would need to be true for something to happen. To my mind, the point of modeling is to ask and answer questions rigorously, and to be explicit about your assumptions. Putting things into numbers and breaking processes into discrete steps forces you to be specific in your thinking and with the story you’re telling, even if the numbers and steps are themselves unspecific.

Because startups are money-losing growth machines by design, lots of traditional financial modeling just doesn’t apply. Too often that means overcompensating and looking at top-line performance absent any more rigorous analysis of what I think of as “sustainability.” Is the growth healthy? People throw around all kinds of terms to asses the health and sustainability of startups. I think it’s mostly bullshit and doesn’t capture or describe anything meaningful.

I’ve found myself increasingly creating models (which again are thinking frameworks rather than predictive tools) to blend together all the various top-line figures into a more-startup oriented version of indicative health. I like to think about things in terms of payback in particular.

To understand why, I’ll use Harry’s as an example.

(Note: all the numbers here are waaaaay off and if this were a real example, there’d obviously be more detail. I’m illustrating a general concept, not proving a specific point.)

Harry’s baseline razor subscription costs $9 per shipment. Let’s assume that the average customer receives 6 shipments before cancelling and that it costs Harry’s $40 to acquire each customer. So each customer represents $54 in revenue and $40 in acquisition costs. Great news! For every $1 you spend on marketing, you get back $1.35 in revenue, a healthy LTV/CAC ratio (lifetime value/customer acquisition costs). You can check the glossary at the bottom for some definitions of terms:

But wait, you might ask, making, storing, and shipping all razors has to cost something too, right? Right. So let’s say all those various supply chain and logistics costs, eat 40% of the revenue (in reality for Harry’s it’s probably closer to 20%). That would mean that Harry’s only keeps 60% of the revenue from each sale, representing $32.40 over the life of each customer. Not as good as it could be but not too shabby…

This is where the math would break down. If each customer is only really worth $32.40 to Harry’s and Harry’s is spending $40 to acquire them, that’s pretty obviously unsustainable. And this is even assuming you know for sure what the customer lifetimes are. Really by the time you do know that, you’re probably not dealing with an early stage startup anymore. So the question becomes “what would have to change for this business to work?”

Here is the general framework I like to use to see all the levers in one place and begin thinking about that question:

To get that lifetime payback (think or this as CAC-burdened lifetime contribution margin or revenue minus acquisition costs minus the costs of the razors, shipping, etc.) into the black, Harry’s could:

Increase order values, either by raising prices or introducing add-on products

Improve contribution margins by lowering some supply chain cost (this is where the line items that make up CoGS matters a lot)

Extend customer lifetimes/improve retention

Lower CAC through better paid marketing or more organic growth

Obviously some of those are easier or more feasible than others. Some may tend to “naturally” (usually that really means a lot of hard work) improve over time and with scale while others may get harder or even worse over time. Where are the reasonable upper limits? What could this reasonably look like? What’s normal? What do we care about? Is this concerning?

There’s no “if X > Y then I must invest” shortcuts or hard and fast rules.

This is where it stops being “financial modeling” and becomes a more creative/intellectual/interesting exercise. But to get here and to be able to answer any of those questions with any semblance of legitimacy and analytical rigor, you have to first ground yourself in a framework. Otherwise it’s just hand-waving. That’s the ultimate point of the exercise.

What this framework also suggests is that to survive, a startup has to be great on one of those levers and to really thrive, it has to be great on two or three. So when I look at a startup, I want to understand where they are today and where they can get on each. Does the prospect of a super sticky product make me relatively indifferent for CAC? Can the margins be strong enough to support low AOVs? So on and so forth.

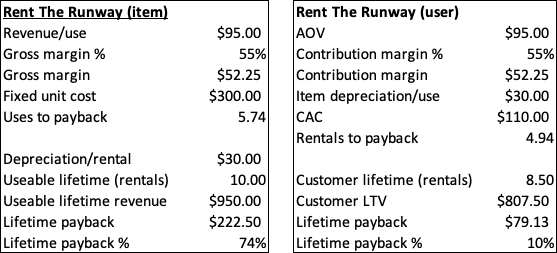

With the appropriate tweaks, this general framework works just as well for consumer startups well outside of subscription CPG. I’ve found it helpful for understanding startups with depreciating assets, lease obligations, software/virtual subscriptions, and one-off/irregular (non-subscription) purchases, etc. And it can work in reverse as well, not just on a per-user basis. Here’s the same type of unit economic model for Rent The Runway:

We’re not talking about top-line growth, and certainly not cash flow or EBITDA. Even once all the numbers in this type of model look good, startups still have to pay their employees, and rent, and lawyers, and consultants, and health benefits, etc. I’m not concerned about profitability as an early stage investor. I care about a path to profitability. Anyone can produce great looking growth by burning enough money. Getting to sustainability is another matter altogether.

To make sense of that and understand it in a meaningful way, you first need to do the work of modeling out both the facts as you them and your judgement as you perceive. Then you can start bending and breaking and hopefully get somewhere.

I’ve put the above models into this Google Sheet. Hopefully I can get around to adding more types of payback models. In the meantime, I would love to hear people’s alternative takes on this.

Am I dumb, wrong, or just pointing out something obvious?

Quick glossary:

AOV: Average order value. How much a customer spends on average each time they buy.

LTV: lifetime value (sometimes CLTV for customer lifetime value). The total amount of money a customer spends over all their purchases: AOV x number of purchases.

CAC/CPA: customer acquisition cost or cost per acquisition. How much it costs (in advertising spend, referral codes, etc.) to get a new customer. These numbers can mean slightly different things in practice but I’m using them interchangeably.

Payback period: the amount of time or number of purchases until you’ve paid back your CPA.

CoGS: cost of goods sold. The cost not just of buying/manufacturing some item but also all the associated variable costs of selling it like storing, packaging, and shipping it.

Contribution margin: the amount of revenue after accounting for CoGS.

Depreciation: how much does the value of something (like a car) decrease over time/with use.

Lifetime payback: this is the metric I’m making up, which works either on a lifetime or transactional basis. It measures (lifetime) revenue minus CoGS minus acquisition costs.