The end of pricing power

Supernovas are the end of a star, after all

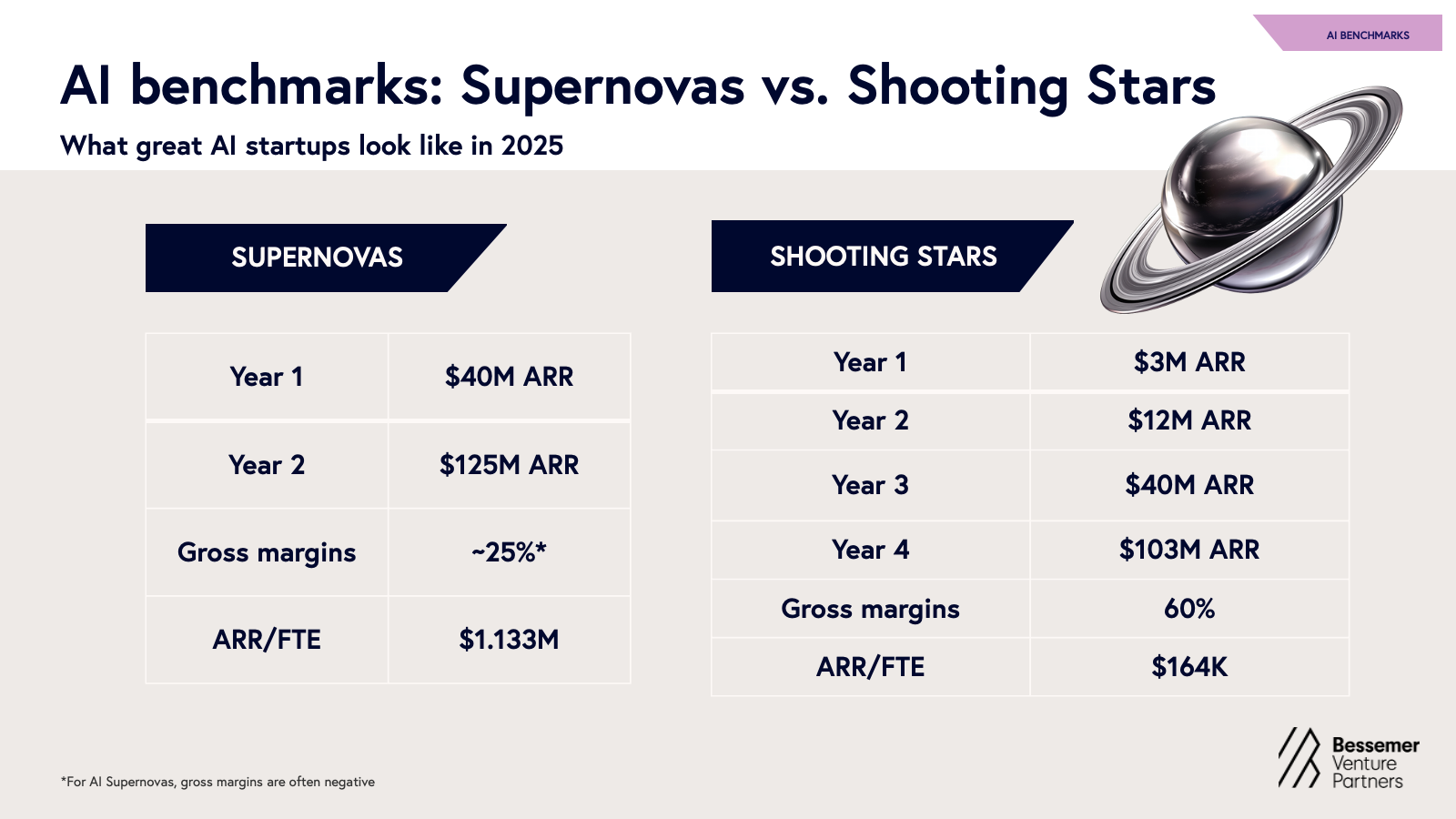

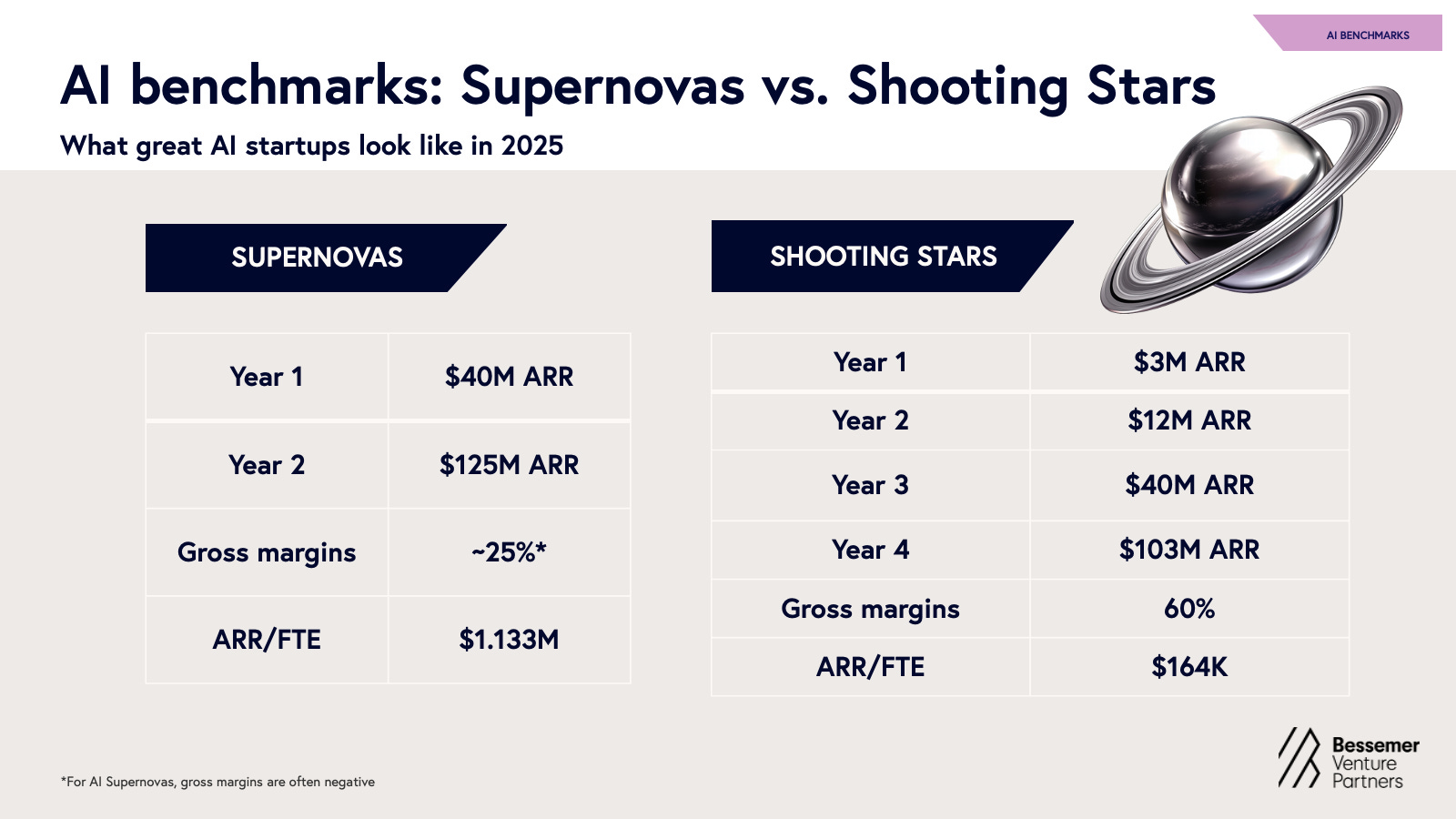

We basically take for granted that good margins = good businesses and bad margins = bad (or at least not-yet-good) businesses. But now negative-gross-margin-but-extremely-fast-growing AI businesses are the hottest game in town - so hot that they even have a name “AI Supernovas.”

{kind=link}

They defy the normal expectations/model of quality and yet everyone loves them.

It’s about time to think about what margins actually mean, what they represent, and why they matter (or don’t).

Fundamentally/definitionally margins represent pricing power. Your ability to extract margins - to charge in excess of your costs - is the definition of pricing power. Pricing power, especially in software businesses, can derive from a combination of places.

The notion of software as a good business with high (gross) margins reflects three assumptions of its operating model:

Zero marginal cost of reproduction (same code, infinite users)

Non-ephemeral value (software doesn't depreciate like media so you can keep selling across time)

High switching costs (mission critical or highly differentiated products drive retention and pricing power)

These all come through as high margins because you can build one thing, sell it to lots of people repeatedly over a long period of time for more than it cost you to build.

Those assumptions undergird everything about how software businesses are planned and run. They are quintessential.

Over time, I think people have tended to focus way too much on #1 and #2 and not nearly enough on #3 as the most significant driver of pricing power and margins.

If you can dictate pricing substantially above your costs without customers leaving/firing you, you have pricing power. You’re capturing value regardless of the business model or usage pattern.

Whether those switching costs derive from brand, network effects, product value, monopoly, transaction/hard costs, or usage/soft costs - doesn’t matter. It shows up in the P&L as margins.

AI changes the equation/exposes flaws in the accepted wisdom:

Marginal costs of reproduction gets worse (still code but now with inference behind it)

Switching costs collapse (less differentiated and easier to swap)

Depreciation accelerates (new stuff gets better faster)

The result: Switching costs decline precipitously and software likely re-equilibrates from 80-90% margins to something much lower. Whether that’s 10% or 60%… who knows.

So what? What are you supposed to do in response?

If the typical drivers of switching costs -> pricing power -> margins deteriorate, you have to find them elsewhere or just be a low value, easily replicated and replaced business.

Go deeper, vertically - Get your hooks in deep such that your customers fully rely on you and switching becomes painful. The worst thing to be is a horizontal point solution (Zoom).

Build for network effects - Create switching costs through networks and “multiplayer mode” such that your value prop gets better with scale and the cost to compete goes up for any new entrant. There’s a reason the only new rideshare competitors have infinite money (Google and Elon).

Roll hybrid models:

Software + services (use services to differentiate software). This is why “forward deployed” businesses are so in vogue right now in the enterprise.

Hardware + software (physical switching costs). You can either generate physical lock in or create proprietary data through sensors, devices, etc.

Services + software (use software to differentiate services). This presents as vertical integration, whether as a de novo business or some kind of acquisition platform.

This isn't just about AI companies having negative gross margins (which is obviously bad business model chicanery and likely fleeting). It's about the fundamental economics of software businesses getting permanently worse and thinking through the logical responses.

Some of the AI companies currently at low or negative margins will win with capital long enough to survive and raise prices. Some of them will ultimately differentiate through some kind of market depth, nfx, or hybrid models. Many of them will die in the crib.

Supernovas don’t last; they burn bright and die.

H/t to Charles Rubenfeld, Tanay Jaipuria, and Caroline Newman for inspiration and bouncing these ideas around with me.

Great stuff as always. One reason I'm bullish on the application layer capturing most of the value is because humans hate change. The invisible stuff like the models might be truly interchangeable but Jeff in accounting at an F500 is not going to want to switch software every 18 months.

Great post. I would add however, that margins are supported by much more than just switching costs. Yes, it does increase pricing power when switching costs are high (see: ERP, CRM, SCM, etc...). However, pricing power and margin resilience are also anchored in ROI demonstrated to customers, regulatory lock-in, unique data assets, network effects, and the business-critical nature of specific workflows. Not all moats are equally vulnerable to the AI margin squeeze. The bigger risk to 50% software companies is the reduction of headcount needed to access the software to conduct jobs --- zero job growth = fewer seats to sell to and a race to the bottom for growth. The hybrid models will evolve the customer's perception of ROI.