Commitment as Leverage

Guest post: The third leg of the stool with code and capital

Editors Note: This a co-authored guest with Alex Barrett, the CEO of Meroka. Meroka is an employee ownership platform for healthcare. Back to our regularly scheduled programming beneath it.

VC and software have PE envy, but they’re doing it wrong

Investors and innovators alike are getting more creative in how they combine financial engineering and software engineering. But in their quest to be puppet master they forget the lifeblood of any business: its employees.

Over the past year there has been lots of attention in VC circles placed on the idea that the next generation of software businesses may look more asset heavy, as there is more value-capture to be had by owning the customer, rather than simply selling to it.

Though not the first to notice, name, or act on this supercycle, Matt Brown summarized it well in “Why VC and Software have PE envy”. Matt argues that innovators and entrepreneurs with a playbook to improve a business have a one-dimensional spectrum of possibilities to improve that business:

On the far left, the traditional PE model uses capital as its main source of leverage by buying businesses and running them, exerting high control, and gaining high value capture. On the far right, the traditional VC model uses code as its main tool by building scalable software that it can license to many users, exposing it to a large market but with low value capture.

Matt gets at what lies between the extremes of this one-dimensional spectrum: strategies in the messy middle combining capital and code to unlock new models.

But the premise of this one-dimensional axis is flawed from the start. The entire spectrum of possibilities here rests on the assumption that we need to engineer these businesses using some outside force (capital or code or some mixture of the two). That the best way to impart a new playbook on a business is to change it, and that changing it requires engineering it, and that we know best how to do that.

Looking at it on a one-dimensional basis does not represent a spectrum of leverage, it represents a spectrum of disempowerment:

On the far left, the traditional PE model (as it exerts high control) operates with the belief that they know how to run the business better than those currently doing it. This typically looks like a team of slick operators taking over key business functions, driving cost optimization as the primary, immediate tool, and taking work away from those in the seats today (either through centralization or staff reduction or both).

On the far right, the traditional VC model (as it seeks ACV) attempts to abstract away as many activities as possible by building software to take those things from those doing the job today. The belief being that software is far more efficient and capable at doing the task than those currently doing it.

While in most cases both of the above are true (the slick operators do figure out some optimization, and the software is more efficient) they both suffer from the same problem in that they accelerate the cycle of disempowerment inside traditional businesses that were built on the backs of work ethic, relationships, and respect for human beings.

Playing the role of puppet master and focusing on how to engineer these businesses from the outside can work. But its value capped because it fails to see the third source of leverage: commitment

Adding commitment as a third source of leverage transforms this spectrum from a one-dimensional to a two-dimensional view, opening up brand new models for innovation. What I’ve labeled above as the “Ownership Model”, which uses commitment as a source of leverage should be familiar to all of us in the technology world who habitually recruit candidates typically out-of-our-league by offering equity stakes, by selling our equity to smart capital allocators, and by using equity as a tool to drive performance and motivate employees.

Commitment does not have a line item in the P&L we can point to. You can’t easily model or forecast it.

Yet it’s the largest source of leverage inside any business. It governs the effort employees deliver, the intentionality of their actions, the quality of their work, and their happiness and satisfaction showing up in the morning. It drives retention, customer satisfaction and productivity in every activity. You better believe it directly impacts the P&L.

Everyone knows and believes in my above sentiments towards commitment and empowerment. It just seems intangible or out-of-our-control as business operators - at least when it relates to others, of course we love our OWN options, and carry. We say things like “work with good people” or “diligence culture” or “make sure you know who you’re getting into bed with”, but why do we feel like this tool is pre-established and out of our control? We believe we can do financial engineering and software engineering all day long, but most lose focus on incentive engineering, the most powerful way of actually making sure the right shit gets done well.

Welcome to Incentive Engineering, writing new rules!

We have much more control over this source of leverage than we think, and many companies have been doing it for years. Let’s explore what the two-dimensional view of business leverage looks like

On the top right of this view, we have combos of traditional PE and ownership models. In the KRR Equity model, firms like KKR have experimented with employee ownership as a vector for stronger growth of their assets. Pete Stavros and his team have formally launched Shared Ownership, a concept that allows employees at KRR-run PE-style businesses to own up to 10% of the businesses they work at. Others in the banking/PE sector have followed through initiatives like Ownership Works. Pushing these models closer to true employee ownership, but still involving capital as a form of leverage are the 7,000 ESOP businesses across the country that have remained independent and allowed their employees to be the acquirers, operators and owners of their businesses.

On the other side of the chart, Ownership models have also pollinated with the traditional VC model. Several companies have built Equity infrastructure related to managing ownership. Most famously, Carta, but more recently (and innovatively), companies like Common Trust have tried to pave the way for any business to adopt employee-ownership as a part of its cultural fabric. Finally, closer to true commitment as a form of leverage, consider the Token economy and how tokens (primarily in the crypto world) use incentive engineering as a way to augment the customer value proposition and increase business value.

But the most powerful approach will combine capital, code and commitment as three tools to impart new playbooks on businesses all across the country. Together, those three levers can transform economics, operations, and incentives from the inside out.

Meroka is pioneering a new model to empower providers and restore the independent practice of medicine. Meroka use capital, code, and commitment as sources of leverage to transform healthcare. Meroka helps medical practices become employee owned AND provides the capital to facilitate the transaction AND builds the technology that improves the practice operations.

Everyone always wants to ask about complexity. “Aren’t you playing on hard mode?!” they say.

Yes, improving businesses is hard, but doing it without the commitment of staff on the ground must be playing on really really REALLY hard mode. By introducing shared upside through equity ownership, Meroka makes the improvement a collaborative process rather than an antagonistic one (PE) or a scope-limited (software) one. We’re working with staff to ensure the businesses thrive, not fighting them or papering over the challenges.

So add commitment to the equation, it changes the game and makes the value creation uncapped.

Conference

On Wednesday we hosted Slow Summer: our annual mini conference for young partners, principals, and EMs.

These are the value- and incentive-aligned partners for us to work with today, and the important leaders in our asset class tomorrow.

I invest often with those running newer funds and my peers building careers in more established ones: leading deals with them, coming in after they do a pre-seed, or supporting them on a smaller round. There’s a spirit of collaboration and open exploration in that room/among that cohort. Everyone is trying to figure it out and aren’t too seasoned or rich be sure we’re right.

The event itself was off the record so I won’t repeat/reveal much - if you want to participate you have to be there - but we had a phenomenal group of speakers:

GPs: Fred Wilson, Lee Linden, Mike Mignano

EMs: Ashley Smith, Ben Braverman, Zoe Weinberg, Nick Chirls, Charley Ma, Blake Robbins

LPs: Paul Mace (Williams), Chris Anderson (TIFF), Jenny Heller (Brandywine)

Much of the conversation centered on the future of the asset class (bifurcation, competition, or something else), firm building (when, how, if to raise), and the first principles of investing (competing, underwriting, and recognizing greatness).

In particular the hour+ long conversation with Fred was a lot of fun. Rarely do I get to chop it on Carlota Perez and get yelled at for (jokingly) referring to an LP as “my boss.”

This is the 5th time in four years I’ve done this event and I’m excited to continue investing in and supporting this network.

I have such tremendous respect for the folks who have been entrepreneurial and gone out to start funds. I learn so much by spending time with them and so excited to continue supporting and working with that community of current and future EMs.

Of course many thanks to Cooley, SVB, and Sydecar for making it possible.

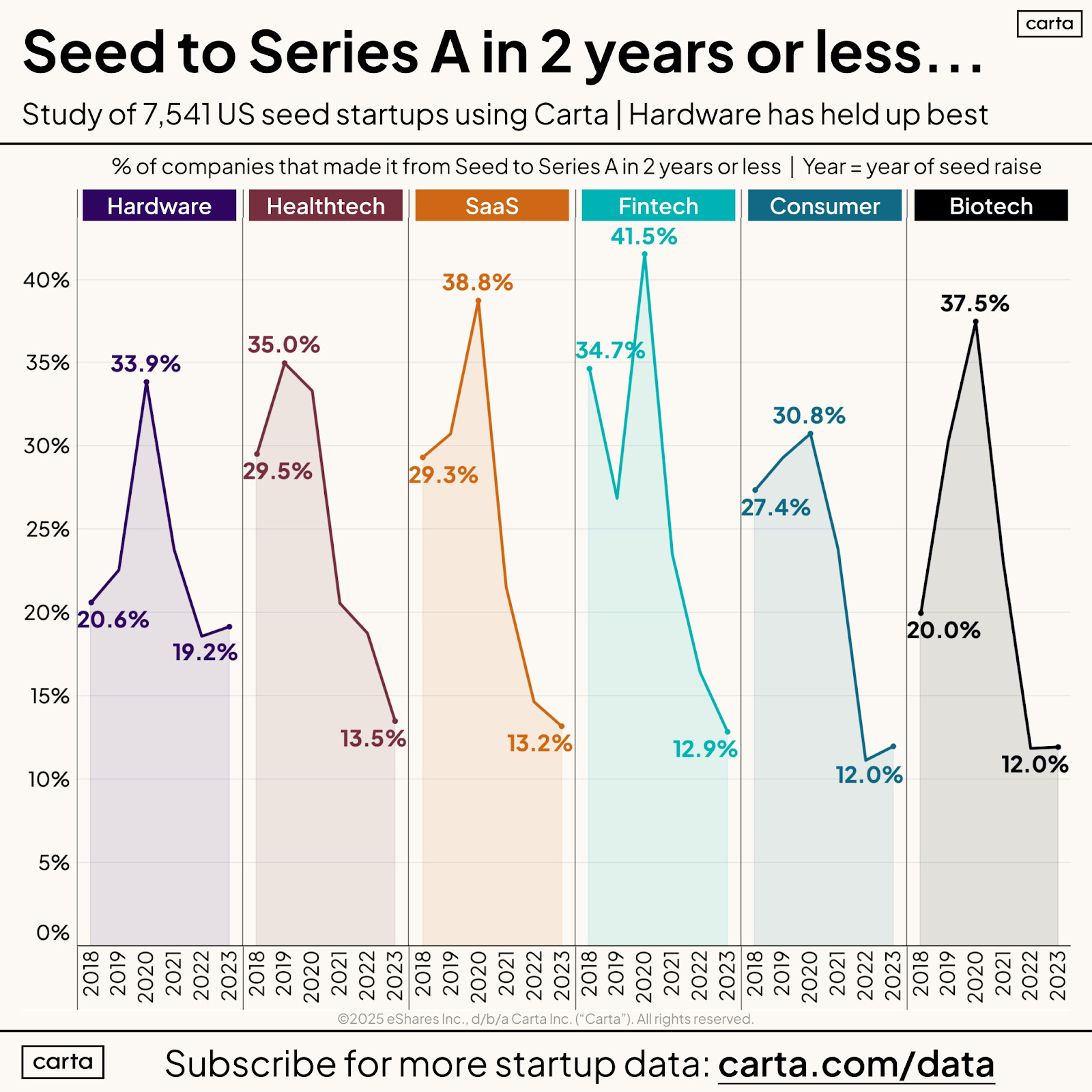

I Read

Good data from Peter Walker/Carta and I really like the take from Jake that Seed companies are just getting overcapitalized and at too high a price. The more you raise and the higher you price it, the higher your expectations are. So at this point the “seed to A” graduation is really more like “Seed to B” all at once in terms of what you need to achieve to raise an A.

Remember, downstream investors want to be able to do rounds at a 2-3x step up from your last round. No one wants to do flat or modest valuation increases. So if you can’t earn that, you’re DOA. That means if you raise $6M on $30M e.g. you have to justify a >$100M valuation just to stay alive.

I Wrote

Are services good now? Sort of but mostly no (if you can avoid it).

I Watched

An absolutely heartbreaking Knicks game. But lest we forget, the Knicks beat the Pacers after the last “choke game.” Fuck Reggie Miller - horrible playcaller. Orange and Blue skies.

The Studio on Apple TV which is a fantastic farce. I heard it described as “Curb on cocaine.”

| A guest post by

|

Alex, I love these thoughts.

1) I think the incentives in this model could be broken down into the jobs to be done by both sides. eg. for PE, the job to be done is to 'buy and run' - how does one incentivise those that buy and those that run so they have ownership? for VC, the job to be done is to 'build and sell' - how does one incentivise those that build and those that sell?

2) To go a layer deeper, monetizing for customers ie. incentives for the recipient of services on the PE side and incentives for the software buyer on the VC side is something that I think about a lot. I think tokenization is the only way to make this work for customers and I'm not sure if it's fits in this model. Would love to understand more about what you are building.

3) I think this also just serves to reinforce the fact that people are in fact the greatest asset (for lack of a better word).